There’s something almost mesmerising about the ongoing rally in global equity markets. Rather than a spectacular race to the peak, this quarter has seen a more slow and steady climb. By the end of March both the S&P/ASX 200 Index in Australia and the S&P 500 Index in the US are reaching new record highs every other day. With interest rates about to start coming down, is there anything to stop the markets climbing higher and higher?

After the exuberance of the “pivot party” in the last eight weeks of 2023 – when central banks all but confirmed that interest rises were over, and the next moves would be downward – many thought that there could be a retraction in early 2024. But markets have shaken off expectations that interest rate cuts are not coming as quickly as they had priced in at the end of last year and have been steadily climbing throughout the quarter approaching their peaks.

Australia’s sharemarket has been touching it’s all time high throughout March, building on the same momentum that has pushed many major global equity benchmarks to fresh records on expectations of a world-wide rate cutting cycle. In the March quarter the S&P/ASX 200 index is up 5.3%, and that’s after the gain of 12.1% between November the 1st and December the 31st last year.

Over the quarter the biggest driver of the Australian stock market has been the banks. The Financial Sector, which makes up 30% of the ASX, is up 12% for the quarter.

However, holding back the market from hitting even higher peaks has been the Materials Sector. This sector – dominated by the big miners – makes up around 22% of the ASX and has been hit hard by falling iron ore and nickel prices.

Pessimism over demand in China has pushed the price of Iron Ore down by 20% in the March quarter. The comes amid continued worries that problems in the construction sector will have long-lasting effects on China’s demand for new property. This in turn has contributed to a negative quarter for the ASX Materials sector, which is down 6.2%.

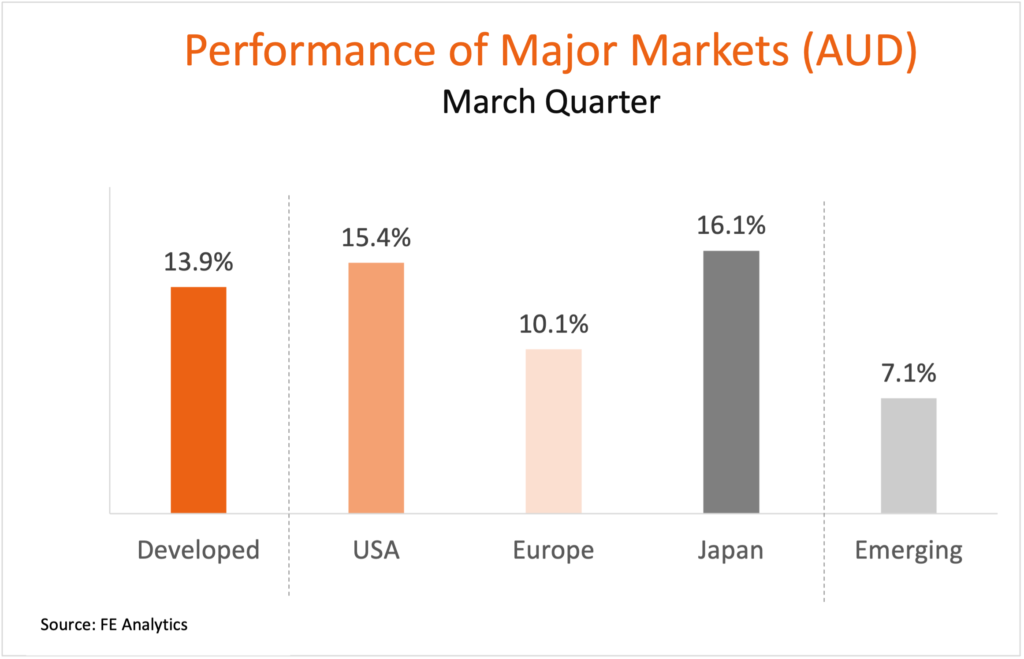

Outside of Australia, the developed markets have seen exceptionally strong returns. The MSCI World Index is up 13.9% for the quarter and a staggering 28.4% for the previous 12 months. Last year the strong global rally in stocks could be put down to a very narrow cohort of large tech stocks – the so-called “Magnificent 7” Nasdaq stocks (Microsoft, Apple, Tesla, Amazon, Nvidia, Alphabet and Meta Platforms). But we are now seeing a broader based rally across markets.

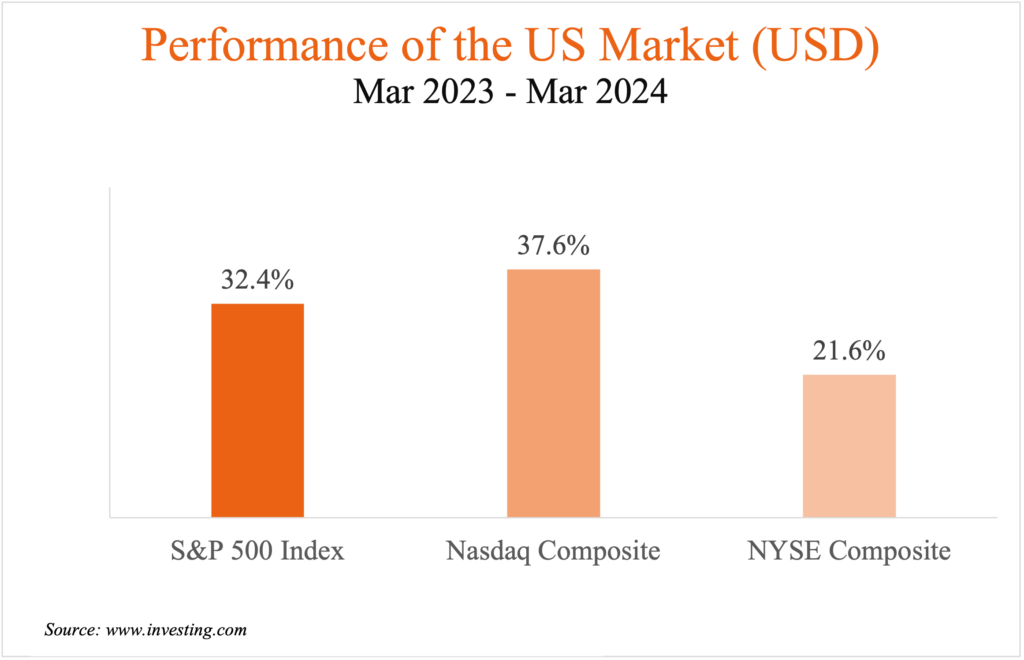

In the US stocks in the S&P500 Index are listed on either the Nasdaq (around 46% by market weight) or the New York Stock Exchange (NYSE). In 2023 the Nasdaq composite index returned a staggering 48% while the NYSE Composite returned a comparatively measly 14% (giving the S&P 500 index an overall return of 28.5% for the year). But this quarter has seen a much more even spread of returns across the two constituent indices, as shown in the chart below.

Furthermore, while the US market is the largest part of the MSCI World Index (making approximately 65% by market cap weight) other major markets have also seen strong returns for the quarter. Europe has returned 10.1% for the quarter and 17.1% for the 12 months (in AUD), while Japan – the perennial laggard of global markets – as returned 16.1% for the quarter and 29.1% for the prior 12 months (n AUD), putting the index within touching distance of the all-time high it hit in 1989.

The Emerging Markets are trailing the Developed Markets, but this is due to the poor performance of China, which makes up around 33% of the MSCI Emerging Market Index. While most major markets have been booming, the MSCI China index has returned 2.3% for the quarter and -14.9% for the prior 12 months.

At the heart of these impressive rallies appears to be the unshakeable belief that a soft landing has been achieved, and that economies will continue to grow. The sharpest increases in interest rates in generations has not led to a recession, inflation has been tamed and continues to fall, moving closer to the 2% to 3% target band that central banks are waiting on, and interest rate cuts are now just a matter of when, not if.

Economic news of the quarter has been consistent with a Goldilocks scenario of continuing growth, low unemployment and falling inflation, with central banks remaining on track for rate cuts this year. However, some market strategists have warned that the market has simply become too overbought and that a material pullback is near. But even they acknowledge it is extremely hard to know how stretched a rally in the stock market has become when the advance is as strong and relentless as this one has been this year.

At this point, it seems there is little to stop this momentum continuing. It’s all blue skies ahead – interest rates and inflation are normalising, economic growth is forecast to improve, unemployment remains low, and there appears to be no obvious risks on the horizon (while acknowledging on-going geopolitical tensions). Of course, these are exactly the times to be cautious about the risks the market doesn’t see coming.

Dr Steve Garth

April 2024